As I warned in my first post on the controlled load shedding that took place in South Australia last Wednesday, there has been near-continuous coverage of the event and the reasons for it, and of course of the subsequent near-misses in NSW (see the collection of Paul’s posts here for how that day evolved, with more to come when we catch our breath).

I’m going to focus here on the reasons given for the gas-fired Pelican Point Power Station in Adelaide not bidding its full capacity into the market on Wednesday 8 February before and during the period when load shedding occurred, despite the fact that it was able to make that capacity available on Thursday evening when “directed” by AEMO.

This is a complex issue and has been the subject of heated debate. Nothing presented here is intended to be conclusive nor exhaustive, but simply an attempt to provide context then dissect and explain a bit more fully some of the information that has so far been put into the public domain.

I would also point readers to a couple of other relevant pieces published recently:

- lawyer Graeme Dennis’s succinct commentary on the NEM rules and gas supply, explaining in general “why gas power stations can’t just be started up straight away”

- energy consultant Hugh Saddler’s broader overview of the reasons for the load shedding published on The Conversation

In this post I’ll be going into more detail on the specific issues affecting Pelican Point. First some background.

Pelican Point PS Configuration

Pelican Point is a gas-fired combined cycle plant built in 1999-2001 comprising two 160 MW gas turbines (GTs) and a 158 MW steam turbine, with a total registered capacity of 478 MW. Each GT directly drives its own generator, and their hot exhaust gases are fed into specialised boilers (“Heat Recovery Steam Generators”) which produce high pressure steam driving the third turbogenerator.

With a single GT operating, the plant is capable of roughly half its nominal output (full GT output plus about half of the steam turbine capacity).

Although there are three physical generating units, for market bidding and dispatch purposes Pelican Point is registered with AEMO as a single “aggregated unit”.

Reduced Operation

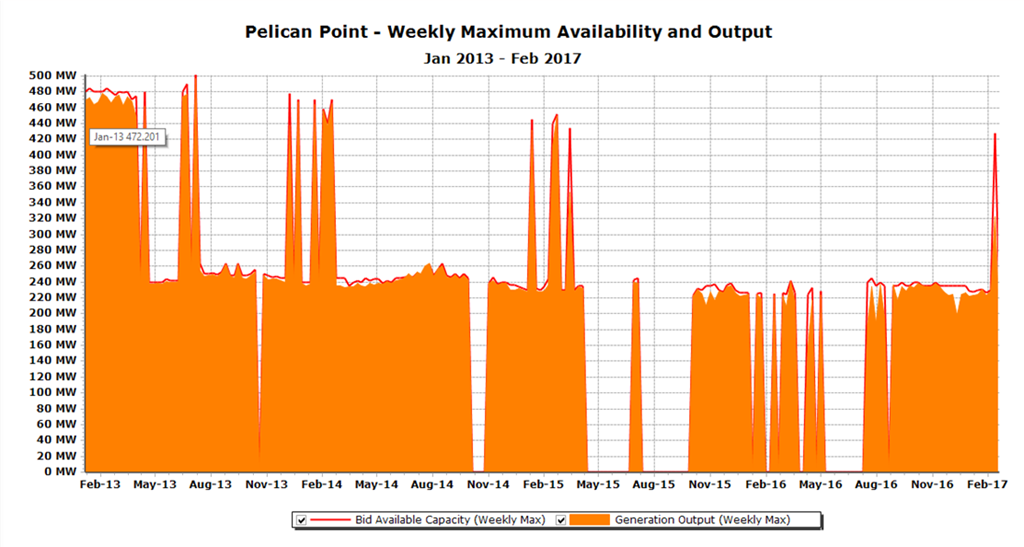

Since early 2013, Pelican Point has operated only rarely at full capacity, and prior to last Friday, not since March 2015, as seen in this chart of weekly maximum availability (ie capacity bid into the NEM) and output from global-roam’s NEM-Review historical market data analysis product:

Pelican Point’s majority owner Engie has stated that there is “no commercial rationale to operate the second Pelican Point unit in the current market environment in SA for a small number of days across the year”.

Thus the station has been operating only a single gas turbine unit supplemented by (up to) half the output of the steam turbogenerator, in total capable of around 220-240 MW under summer conditions – slightly more output is available in winter.

Gas Supply and Transportation

Gas for the station can be delivered from either the Moomba to Adelaide pipeline (MAPS) carrying gas from the Cooper Basin, or the SEA Gas pipeline carrying gas from western Victoria.

A critical factor for gas powered generators is the maximum rate at which they can draw gas from their supplying pipeline system(s), generally specified in terms of a Maximum Hourly Quantity of gas, or MHQ. Physically, the rate at which a station like Pelican Point draws gas is broadly proportional to its current output. Commercially, the station must have rights under its gas supply and transportation arrangements to use gas at that rate. Although we obviously do not have information on Engie’s specific arrangements, in general on long distance commercial pipelines such as MAPS and SEA Gas, if a pipeline user with a contracted level of supply takes gas at rates exceeding their maximum right to MHQ for any length of time, they will almost certainly be in breach of their contract conditions, face material contractual cost penalties (“overrun charges”) and be at some risk of having gas supply physically curtailed.

The same media release linked to above states that “the second Pelican Point unit has no gas contracts in place”. In practice, gas contracts would not be particular to operation of a specific GT unit at Pelican Point, so my interpretation of Engie’s statement is that its current gas supply and transportation arrangements only provide enough MHQ to operate one GT at its full output.

Bidding and Dispatching Additional Capacity into the NEM

Engie’s statement includes the following critical sentence:

“Under the National Electricity Market (NEM) rules, generators can not bid plant into the market if supply can’t be guaranteed”

** I am not in a position to comment in detail on this statement which would require a closer scrutiny of the National Electricity Rules and other data than time allows. However it appears entirely logical, since the market’s real time dispatch processes necessarily assume that generator bids are capable of being fulfilled – ie following AEMO’s dispatch instructions – immediately they are called upon. For the purposes of this analysis I shall assume Engie’s statement is an accurate reflection of the market rules. **

The important implication of this statement and the considerations above is that in order to bid more Pelican Point capacity than available from running one GT, Engie would need certainty of access to additional MHQ.

To run Pelican Point at higher output levels requires two GT units in service and would require drawing gas at higher hourly rates. To allow this, the station would have to enter into some form of additional gas supply and transportation deal(s) to contractually support these higher rates. Such deals could be longer term contracts for increased amounts of gas and / or transportation, or possibly short term “spot” deals with either the pipeline operator and / or another gas user holding supply and transportation rights. But note that there is no guarantee that either form of deal – particularly a short term (and almost certainly short-notice) spot arrangement can be negotiated on acceptable commercial terms as and when required.

Another key point here is that either form of deal would require an increased financial commitment to pay for rights to additional gas and / or transportation – at least part of which would be payable whether or not the additional plant capacity was dispatched and those rights therefore used.

Based on its media statement, Engie clearly judged some time ago that entering longer term contracts for MHQ beyond operation of one GT was not commercial. This left only the shorter term “spot” gas deal as a possible option for bidding and running more than one GT on a particular day or days last week.

Why didn’t Engie do this last Wednesday?

Market Outlook for SA, Wednesday Feb 8

One answer might be that no such spot gas deal was possible in the timeframe required.

Another might be that based on conditions at the time that any deal might have been needed and able to be negotiated, the market outlook did not lead Engie to decide that this was likely to be commercial. We have to remember that the NEM is broadly designed to work through its participants making commercial judgements – which may prove sound or otherwise – in response to price signals, within the manifold rules of the market. AEMO is ultimately responsible for overseeing and maintaining system security and has various powers of intervention, direction and so forth if it judges that participants’ commercial actions and likely market responses are insufficient to deliver that system security.

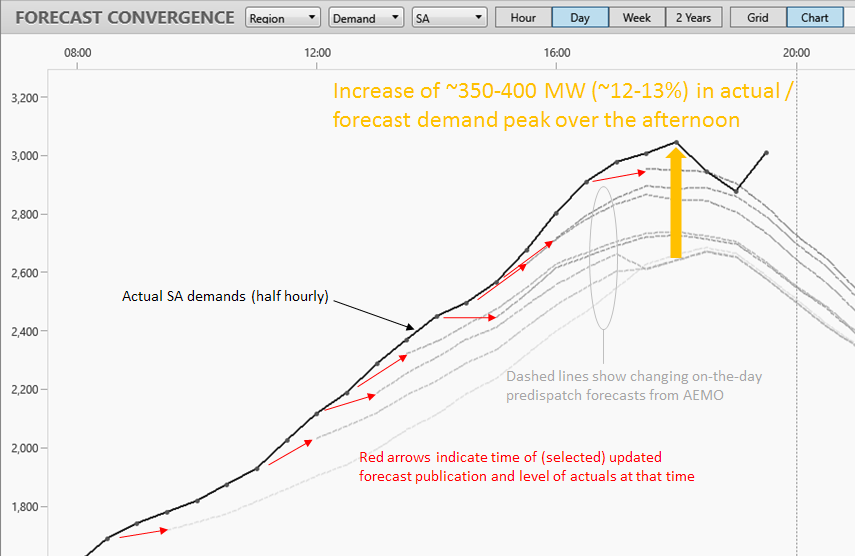

Here’s a chart from the earlier post looking at Feb 8, using ez2view’s Forecast Convergence tool to show how AEMO’s demand forecasts for South Australia evolved on the day:

The key takeout from this chart is how AEMO’s predispatch demand forecasts, updated every half hour through the day, systematically underestimated actual demand outcomes and even late in the afternoon did not foresee the continuing rapid rise in demand which by 6pm forced load shedding to maintain system security (all times are NEM time, AEST, and so half an hour earlier than Adelaide daylight saving time).

From market participants’ perspective, AEMO’s accompanying predispatch price forecasts, shown here in ez2view’s Forecast Convergence grid view, are an important commercial indicator:

This chart shows the evolution of successive on the day price forecasts made between 2pm and 6pm, for the period out to about 10pm. Before 3pm, extreme 5-digit prices were not being forecast by the market systems, with maximum afternoon prices showing as around $300-$600/MWh. If Engie had been seeking to offer additional generation capacity from Pelican Point by late in the afternoon, by 3pm, or probably even earlier, it almost certainly would need to have arranged additional gas & transportation and commenced readying its second unit for startup.

And whilst ongoing spot prices of $300 – $600/MWh would be very profitable for operation of a CCGT plant like Pelican Point at gas prices even up to $20-30/GJ, the logistics, economics, and risks of arranging short term spot gas supply (if possible) then starting and stopping a second GT for a forecast short run of only a few hours at such prices – which were not necessarily certain to occur – evidently didn’t seem compelling to Engie.

In any case it is clear that on the day Engie did not prearrange additional gas enabling it to offer to the market capacity beyond one GT.

None of this is to say that Engie’s decisions prior to or on the day were correct, incorrect, <insert adjective of choice here> … The purpose of the above analysis is to look more deeply at the factors and constraints acting on their decision and ability to offer or not offer that capacity under the market rules.

AEMO Direction – 9 February

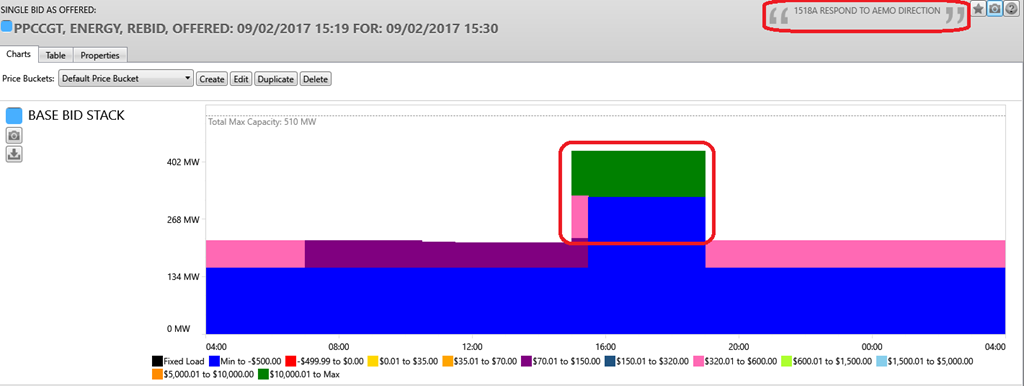

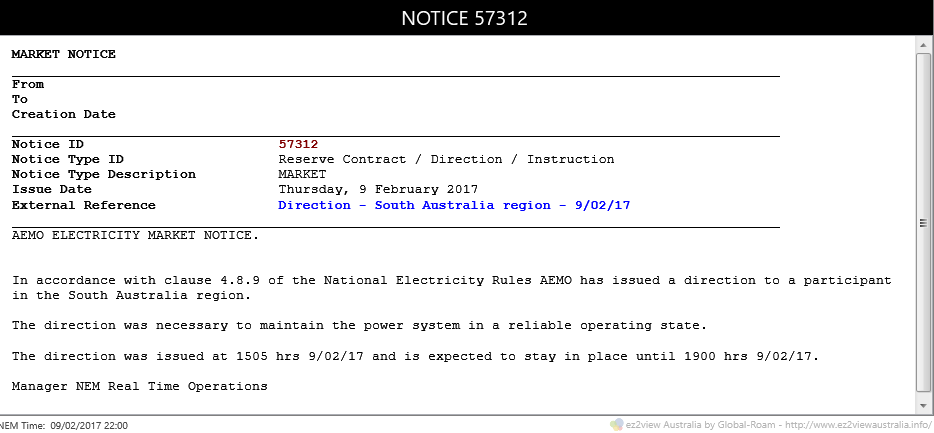

Finally, we also know from Engie’s media statement that on Thursday 9 February capacity from the second GT unit was made available, following a direction from AEMO – here is the capacity rebid seen in ez2view’s Bid Details widget:

AEMO’s relevant market notice shows that this direction was formally made at 15:05 NEM time, although there had presumably been discussions throughout the day to ensure that the direction was capable of being followed – including confirming that additional short term gas supply could be arranged.

Under Direction from AEMO, a participant is entitled to recovery of its net costs, regardless of market price outcomes, with Engie’s media release emphasising this point:

“However, once ENGIE was directed on by AEMO on February 9, we were able to promptly start the second unit, ensuring our costs were covered, including gas to operate the unit.”

All this tends to confirm that the decision not to offer the unit on February 8 was a commercial one, particularly centring around gas supply considerations.

|

Allan O’Neil has worked in Australia’s wholesale energy markets since their creation in the mid-1990’s, in trading, risk management, forecasting and analytical roles with major NEM electricity and gas retail and generation companies. He is now an independent energy markets consultant, working with clients on projects across a spectrum of wholesale, retail, electricity and gas issues.

You can view Allan’s LinkedIn profile here. Allan will be regularly reviewing market events here on WattClarity. Allan has also begun providing an on-site educational service covering how spot prices are set in the NEM, and other important aspects of the physical electricity market – further details here. |

So systematic market failure where the market does not provide incentives for efficient large generators to run when they are needed. Instead of trying to come up with an extremely elaborate market mechanism to balance all of these competing interests, we should nationalise them and take the profit motive out, so that we have the capacity when we need it. Natural monopolies like all utilities markets, can’t be engineered into a competitive market.

The fact that this is also happening in NSW and QLD shows it is an issue with the market structure and likely also rational self interested actors gaming the system.

I find it odd that small inefficient generators in SA can continually run making profit but large efficient generators can’t.

If we nationalised, we would just be facing government failure instead of market failure. Why do you assume a nationalised system would work better given governments’ track records? Why do you believe that government’s don’t face their own financial constraints that will influence how much they are prepared to invest in the system? How do small scale alternatives to grid electricity like solar and battery fit in? should we nationalise these too? If not, why not? And given solar is already competitive and some argue that in SA at least, batteries are too, then perhaps we are no longer in the situation of a “natural monopoly”.

Well said Kieran.

I don’t assume that you won’t have issues with government failure, nor that they won’t have their own constraints. More so, they would have LESS constraints than an ordinary business. Solar and battery are independent, like running a generator for your own home, you’re trying to increase the scope there by likening a 5KW generator to a 50,000KW generator. The market is still a natural monopoly, particularly with distribution.

Every issue you’ve brought up is a problem under a market system as well, except under a market system you’ve also got the additional issues of regulatory capture and gaming the system.

Markets aren’t magic.

“Solar and battery are independent, like running a generator for your own home..”

True but that’s a rare situation wrt the communal grid whereby there are lots of rooftop solar generators with no storage capacity bludging off the insurance of the grid and paying no insurance premiums. Quite the contrary as many are being actively subsidised to bludge off the grid like mine is.

Uriah & Kieran

Putting aside the public / private ownership question, a different issue worth considering is the generation technology mix in South Australia (and elsewhere in the NEM). While large scale combined cycle gas plants are thermally efficient, they are not nearly as flexible as some other forms of generation particularly with rising gas prices and increased amounts of variable renewable generation pushing them towards peaking / reserve operation. Here I mean “flexible” in an economic sense as much as an operational one (however CCGT plant is generally less flexible in terms of startup time, minimum run time etc than open cycle turbines).

We can see this in the decision by Engie to reduce the quantity of gas contracted for the station. Contracting gas supply and transportation for the full plant capacity would involve committing to higher fixed costs, with an uncertain likelihood of recovering these costs from a limited number of opportunities to run economically at full capacity (due to high running costs on gas which has become a much more expensive fuel than it was when Pelican Point was built, versus the very low marginal cost of renewables).

Regardless of who owns Pelican Point this underlying economic shift creates a difficulty in economically optimising the operation of a station like this and maximising its value to the system. For true peaking / reserve operation in an environment of high gas prices, the best form of “gas-fired” plant might actually be open cycle turbines running on liquid fuel – the lower fixed costs of both the generation plant and fuel supply outweighing the higher costs of relatively infrequent running. Hence “small inefficient generators” running “profitably” and Pelican Point at only half capacity!

Allan

Some people are pointing fingers at the wind power lull, but it is the wind power peaks that have killed the concept of “baseload” in South Australia. Generators like Pelican Point and Osborne operate in baseload mode, maintaining steady output, between infrequent step changes. In recent years baseload generators have been often kicked off the system by wind power surges, so its not surprising that some have closed or been mothballed. Ordering loss making generators to be on standby does not seem like a complete solution.

A major long-term problem for SA is keeping Torrens power station in operation, it is the workhorse load-follower, surely the most important electricity asset in the state.

Thankyou for an excellent and easy to read analysis of what happened with lack of supply from Pelican Point.

So, at the end of the day, if a generator can’t guarantee that it will make its money back on providing electricity to the grid, it won’t, unless they are directed to by the AEMO in which case any excess charges will be covered.

Sounds fair to me – they are not operating as charities, or even as public services.

Also sounds like a failure of the AEMO to predict usage.

How much of the planning and foundations of the NEM took the impact of secondary suppliers’ pricing into account when the national model was developed? Are there just too many links in the profit chain?

“Under the National Electricity Market (NEM) rules, generators can not bid plant into the market if supply can’t be guaranteed”

What a laugh that is with renewables and until the AEMO has the power to restrict any tenderer of electrons to the communal grid to the maximum they can guarantee 24/7, all year round this Govt sponsored form of domestic dumping will continue without a level playing field that consumers require. If that mandate was implemented, then renewables would either have to partner with thermals to lift their average tender rates and/or invest in storage, whereas at present they’re freeloading on thermals as insurers and not paying them their just premiums. What a crock that is and the ACCC would normally have the power to jump on such dumping practices should it occur.

A simple analogy would suffice if say a Labor Govt wanted to privatise the Fire Brigade and proudly announced the CFMEU tender was the lowest priced and has been accepted. Just a wee problem in the fine print folks. There won’t be any fireys on duty when the sun goes down and/or there’s no wind or wind over 90km/hr. Yeah right!

So you’re saying small gas generators that have low start up costs by higher operating prices should not be allowed to turn on in peak periods and off in low periods? You’re saying when gas prices go up and they need to shut down, they should be forced to stay on?

I’m just drawing a comparison with your standard for wind and applying it to gas as well. Small generators have a benefit over large generators in some regards, so the large ones are “insuring” the small ones. This isn’t unique to wind.

Fluctuations happen in resources and these have flow on effects. You can debate over their size, but that’s about it.

“So you’re saying small gas generators that have low start up costs by higher operating prices should not be allowed to turn on in peak periods and off in low periods?”

No I’m not saying that at all because clearly those gas peaking plants, short of a breakdown, can produce up to their maximum output anytime demand and pricing calls them forth. OTOH they couldn’t match a base load cogen gas plant like Pelican Point that would have long term gas contracts for the whole of their plant and it would be up and running and rather than 6 hours lead time to fire up the idle generator that could easily ramp up output with both gas generators already operating. That’s because they’d either be insuring fickle wind and solar and getting their just insurance premiums, and/or the unreliables would be paying for battery, hydro or molten salt storage in order to compete on a level playing field.

We need high priced peaking gas plants too but what we don’t want is fickle generators dumping in any part of this grid equation.

“I’m just drawing a comparison with your standard for wind and applying it to gas as well.”

Actually on that point there’s no reason why it shouldn’t also apply to large base load plants like Pelican Point too. ie under their 24/7 all year round maximum they wish to guarantee to the AEMO they’d have to in turn partner with fast start gas peaking plants to insure them. Nevertheless creating a level playing field would largely impact the unreliables who are at the mercy of the elements and rightly so if we as consumers aren’t to be.

Err guys, try ruling an average 30% average line through this graph and then imagine the wind turbine industry not being able to tender any power above the line and having to make up any power below the line- http://anero.id/energy/wind-energy/2017/february

Get the picture?

Not to worry folks the CFMEU Fire Brigade quote includes an ironclad guarantee only union fireys will be employed, whereas the other nasty capitalist tenderers won’t guarantee that 😉

Here’s the big storage problem for solar-

http://breakingenergy.com/2014/10/29/at-ivanpah-solar-power-plant-energy-production-falling-well-short-of-expectations/

http://www.powermag.com/crescent-dunes-solar-energy-project-tonopah-nevada-2/?pagenum=1

and ditto wind with any mandated level playing field which is why State Govt’s like SA refuse to acknowledge what’s been going on, but with base load coal increasingly being run on sticky tape and string to extract the last bit of revenue out of them before they shut down, their day of reckoning is fast approaching.

Roger, I think you make some good points. Its a pity you use such a belligerent style — it detracts from your essential points. That we pay the same $ per MWh for dispatchable energy as we do for semi-scheduled and non-scheduled energy seems to not be a proper recognition of the value of the energy offered. Because of the variability of both sources it increases the daily range and variability that the load following plant has to account for, and its more expensive for that plant to operate in that environment. As we see here in Allan’s excellent analysis of Pelican point. It seems inappropriate to me that the generators that contribute to the creation spikes by their variability, also enjoy the high prices. Because wind and solar gets “dispatched” first, and gets paid the spot price price, there is no incentive for them to invest in storage of some sort. If there was some discount from the spot price to reflect their non-dispatchable nature it would encourage storage.

Mate, I get belligerent when the lights go out because too many technical experts have been too nice for too long, while belligerent watermelons have cowed them into shutting up and going along for the ride as they foist their theories and unreliables on us all as consumers. To put it bluntly to these leftys who turned their red coats inside out to wear the green on the outside when the Berlin wall fell and their ideology was in tatters, all electrons are equal, but some are more equal than others. Ipso facto I gave you the only rational, sensible way to make them all equal, whatever the world’s omniscient guru thinks should be the same tax price for all to price their input CO2, in order to get the world’s atmospheric CO2 back to the level the omniscient guru knows it really should be. I am not that guru but I sure as Hell know unequal electrons when I see them and the time for pleasantries is over.

Roger S:

The NEM is not a creature of the environmental movement, but of economists. The environmental movement has been advocating markedly different strategic policies in this sector for more than 40 years. Governments have preferred to take their advice from economists and the conservative press and have failed to predict or to plan for the train wreck that is now coming upon us at full steam.

A coherent policy has been made difficult if not impossible by the fragmentation forced upon the sector by vocal advocates of competitive free markets in the conservative press and conservative think tanks.

Question for you: Who is able to effect fundamental reform of the National Electricity Market? Who is in charge of the regime? It certainly ain’t the environmental movement.

Chris

Thanks for your comment.

While it’s true that within any given half hourly settlement period all generators earn the same spot price for their output (before adjustment for locational network loss factors), the average price that different generators earn across a given day, week, etc can vary widely depending on how each generator’s output moves as the spot price changes.

Taking just the 8 hour period midday – 8pm in SA on the day of load shedding, wind generators’ output fell steadily through the afternoon, while thermal generation ramped up to fill the gap and meet (not quite, unfortunately) the increasing demand (see https://wattclarity.com.au/2017/02/initial-analysis-sa-load-shedding-wed-8-feb-2017/ for a chart showing this). Prices in this period rose from a few hundred dollars per MWh up to the Market Price Cap of $14,000/MWh whilst load was being shed.

The demand-weighted average spot price over this period was $4,642/MWh. Wind generators as a group, with much more of their output occurring before the price spiked and much less during the period of extreme prices, earned an average price of $1,584/MWh, a 66% discount, while thermal generators as a group earned $5,206/MWh, a 12% premium. Within that thermal group, generation that ramped up specifically for the extreme price period would have earned a much larger premium.

This is an extreme example, but it clearly shows that the spot market – as intended – does send price signals rewarding dispatchable generation able to contribute more during periods of tight supply-demand balance. Previously on WattClarity, Paul has posted some interesting articles including this one commenting on the increasing discount to average spot prices being earned by windfarms in South Australia.

Aside from the energy price, there are other mechanisms – principally the markets for Frequency Control Ancillary Services – that can reward / penalise generators for ability or lack thereof to contribute to stabilising system frequency etc, again related to the “controllability” of those generators’ output. This is an active area of debate and development in the NEM, as the need for and nature of the services required changes within a transitioning system.

Allan

Hi Allan,

Thanks for taking the time to explain that not so obvious effect of averaging, and that it does create an incentive for dispatchable generation, and therefore for storage. Thinking about the main thrust of your article, the day ahead bidding requirement makes it quite awkward for generators that are market exposed for their fuel cost. I suppose this would be similar for pumped hydro, because their fuel, the power to fill their upper reservoir is also market exposed. For a large pumped hydro with a daily charge/recharge cycle, the day ahead bidding would require them to bid to sell energy they haven’t secured yet. To charge the upper tank they would be bidding as dispatchable load, and if their bid mean they did not get dispatched as a load, they then would not be able available to generate. That seems to place them in the same predicament as Engie, having uncertainty at both buying and selling. On the other hand, smaller unscheduled generators don’t have to commit ahead of time, and can respond the actual market price at the time, a much safer alternative, than having to commit in advance. The playing field seems quite in need of some levelling.

I have an idea, it comes from recycling something that worked.

Lets look at what the SECV did successfully for 85 years.

Take the profiteering out of the equation and treat it as an essential service

So there seems to be a lot of conflicting information.

http://www.afr.com/news/politics/wind-and-thermal-generators-failed-sa-in-blackout-says-aemo-20170215-gudbkq

http://www.joshfrydenberg.com.au/guest/mediaReleasesDetails.aspx?id=304

But the fact remains that Pelican Point could have been on in less than 15 minutes, so I’m still not sure what was at play.

Looks like Pelican Point is back in the market at full capacity, as previously modelled by AEMO as a result of Hazelwood closure. Currently outputting approx 420MW. Haven’t seen any official announcement yet.