As part of the organisation’s energy leadership ambitions, The University of Queensland (UQ) installed the state’s largest behind-the-meter battery in late 2019. The 1.1MW / 2.15MWh Tesla Powerpack system accompanied UQ’s move to be the first university in Australia to participate directly in the wholesale electricity spot market. At an all-in cost of $2.05 million ($953/kWh), the project was funded through the sale of renewable energy certificates created by UQ’s existing 6.3MW behind-the-meter solar PV portfolio.

As a teaching and research driven organisation, UQ is keen to share the learnings and outcomes of this project (which was primarily developed for commercial purposes) in an open and transparent manner, including an assessment of actual performance against business case assumptions. The full report on the battery’s business case and Q1 performance is due to be launched in mid-May and will cover these issues in depth. This article is an extract of the report and explores the battery’s performance during Q1 2020 regarding the ‘virtual cap contract’ service that it can provide.

A free webinar to present the report and hold a Q&A session will be held at 1pm Friday 22 May. Register here.

Background

The UQ battery has been developed to deliver revenue and value from the stacking of four distinct services:

1. Arbitrage

A custom developed control system (the Demand Response Engine or DRE) aims to charge the battery when prices are low and discharge when prices are high – maximising the ‘spread’ between prices to help offset energy costs while respecting the fact that the battery only has a finite storage capacity (roughly two hours at full power).

2. Contingency FCAS

Through a partnership with Enel X, the battery is paid to remain on standby to respond to sudden disturbances to grid frequency from events such as power plants tripping offline or storms damaging transmission lines. Revenue is earnt by bidding this response capability into the NEM’s three contingency Frequency Control Ancillary Services (FCAS) markets – Raise 6 seconds, Raise 60 seconds, and Raise 5 minutes.

3.Peak demand lopping

It is intended that the battery will help UQ to reduce its monthly peak demand charges by lopping the top off the highest metered demand intervals of each month. The control strategy that enables this functionality was not completed in time for Q1 2020 and is discussed further in the full report.

4. ‘Virtual’ Cap Contract

The fourth and final service is the use of the battery as a form of ‘virtual’ cap contract – helping to manage spot price risk in place of a more traditional financial cap product.

The ‘Virtual Cap Contract’ Concept

As a participant in the wholesale electricity spot market, UQ is required to develop risk management strategies to the potential impacts of market volatility. One option available to help manage this risk is the use of ‘cap’ contracts. These financial products act as a form of insurance against extreme market prices. The buyer of the cap contract pays a ‘premium’ (typically expressed as $/MWh for a fixed volume) and is ‘paid out’ if and when market prices exceed a set threshold. This threshold is typically $300/MWh, and the payout is calculated on the difference between this level and the spot price for the relevant interval. For example, if the spot price in a half hour interval was $2,500/MWh, the cap contract holder would be paid out $2,500 subtract $300 (i.e. $2,200/MWh) multiplied by the volume of the cap contract held. At the end of a defined period (e.g. a quarter), the cost of the premium minus the revenue from any intervals where the contract paid out is the net value of the cap contract to the holder.

As a behind-the-meter asset that is able to respond quickly to market price spikes, the UQ battery is able to replicate the risk management function performed by a financial cap contract at least partially. This ‘virtual’ cap contract function works by the battery discharging stored energy during intervals where prices spike beyond a set threshold (e.g. $300/MWh). This then reduces UQ’s load by 1.11 MW and thus UQ’s exposure to the high market price by the same volume

The primary shortfall of a virtual cap versus a financial cap is that it is unlikely the battery will be able to respond to every price spike in a way that provides coverage for the full half hour interval. This is largely a function of the NEM’s current 5/30 settlement dynamics, where dispatch spot prices are set every 5 minutes, but trading prices (which are used for financial settlement) are based on the half hourly average of six dispatch prices. This can result in scenarios where the 5-minute dispatch price unexpectedly spikes mid-way through a 30-minute interval, leaving UQ partially exposed to the high price, even if the battery responds immediately and discharges for the remainder of the half hour. The virtual cap contract is also subject to many of the same constraints as the battery’s other services – namely physical limitations on the duration of energy storage. This means that coverage may fall short during periods of prolonged market volatility as the battery’s stored energy depletes. On the other hand, the primary benefit of a virtual cap is that once the capital cost of the battery has been expended, there is no ongoing premium payable for this service like there would be for a financial cap.

It is worth noting that the need for hedging such as a financial or virtual cap contract arises due to the fact that a sizeable portion of UQ’s load is ‘essential’ and unable to be curtailed if and when high spot prices arise. Notwithstanding this, the use of the Demand Response Engine to autonomously and actively manage the parts of the organisation’s load that do have some degree of flexibility is a key focus of current efforts. and will be explored in a future WattClarity article.

Calculation Methodology

The net value of the virtual cap contract to UQ needs to be calculated with reference to the appropriate avoided cost of using this in lieu of a financial cap. This requires the net value of a hypothetical financial cap contract to be calculated for comparison purposes. The first step to do this is to determine the gross cost of its premium over the quarter. In this case, a rate of $12.37/MWh has been used, being the average price of Q1 2020 cap contracts from the ASX Energy exchange as traded during the three months preceding the start of Q1 2020. Gross income from the pay out of the contract in all intervals greater than $300/MWh is then subtracted from this premium to determine the net value of the financial cap over the quarter.

The value of a virtual cap can then be determined by comparing it to the financial alternative over the same period. This is done by first calculating the costs incurred by the virtual cap in the periods where full ‘cover’ was not provided. For example, in an interval where the spot price was $1,500/MWh, a financial cap would have paid out $1,200/MWh multiplied by the cap volume (in this case, 1.11 MW or 0.555 MWh per half hour). If in the same interval the battery was only able to respond and discharge for 20 out of the 30 minutes, there would be a 0.185 MWh shortfall which would carry with it a cost ‘penalty’ of $222 for the interval.

The overall value from the battery’s virtual cap service is then calculated from the difference between the net cost of the hypothetical financial cap of the same size subtract the sum of the virtual cap cost penalties over the same period. Refer below for the specifics of the calculation for Q1 2020.

Note that no cost or revenue from the energy associated with charging or discharging the battery is attributed to the revenue figures provided for the virtual cap contract service. This is due to these values already being captured in the methodology which calculates the total revenue of the arbitrage value stream. As a result, including the value of energy brought or sold due to the virtual cap contract service would be double counting.

Q1 2020 Performance

It has been calculated that a 1.11 MW financial cap contract would have represented a net cost to UQ of $22,804 over the quarter. This is comprised of $29,995 of gross premium cost subtract $7,190 of income from the payout of the contract across the 18 intervals that exceeded $300/MWh during the quarter.

During this same period, the virtual cap resulted in a cost to UQ of $3,389 based on the shortfall in its coverage of high price intervals. In total, the virtual cap provided 5.79 MWh of coverage out of an overall total of 9.99 MWh of exposure across the 18 intervals – equivalent to coverage of 58% on a volume basis. An alternative performance metric is to assess the percentage of cover provided on a financial basis. That is, did the periods of missed coverage skew towards being relatively higher or lower priced? This is an important question, as faced with only limited discharge duration the battery should theoretically prioritise covering those intervals that are higher priced. In reality however – and for the reasons discussed further below – coverage on a financial basis was lower than that on a volume basis, at only 53%.

Overall the virtual cap service delivered $19,415 in net value to UQ across Q1 2020 compared to a financial cap alternative – the $22,804 avoided cost of a financial cap subtract the $3,389 penalty of missed coverage.

Full results broken down by month are provided in Table 1, noting that costs are represented as negative values.

| January | February | March | Total | |

| Financial cap gross premium | -$10,218 | -$9,559 | -$10,218 | -$29,995 |

| Financial cap gross income | $6,923 | $27 | $241 | $7,191 |

| Financial cap net value | -$3,295 | -$9,532 | -$9,977 | -$22,804 |

| # of intervals above $300/MWh | 15 | 1 | 2 | 18 |

| Max. potential exposure MWh | 8.325 | 0.555 | 1.11 | 9.99 |

| Max. potential exposure $ | -$6,922 | -$27 | -$241 | -$7,190 |

| MWh covered by battery | 4.231 | 0.455 | 1.101 | 5.787 |

| MWh left exposed | 4.094 | 0.100 | 0.009 | 4.203 |

| % volume cover by battery | 50.8% | 82.0% | 99.2% | 57.9% |

| Cost of virtual cap missed coverage | -$3,381 | -$5 | -$3 | -$3,389 |

| % financial cover by battery | 51.2% | 81.5% | 98.8% | 52.9% |

| Net value of virtual cap vs. financial cap | -$86 | $9,527 | $9,974 | $19,415 |

Table 1: Summary of virtual cap key performance figures by month

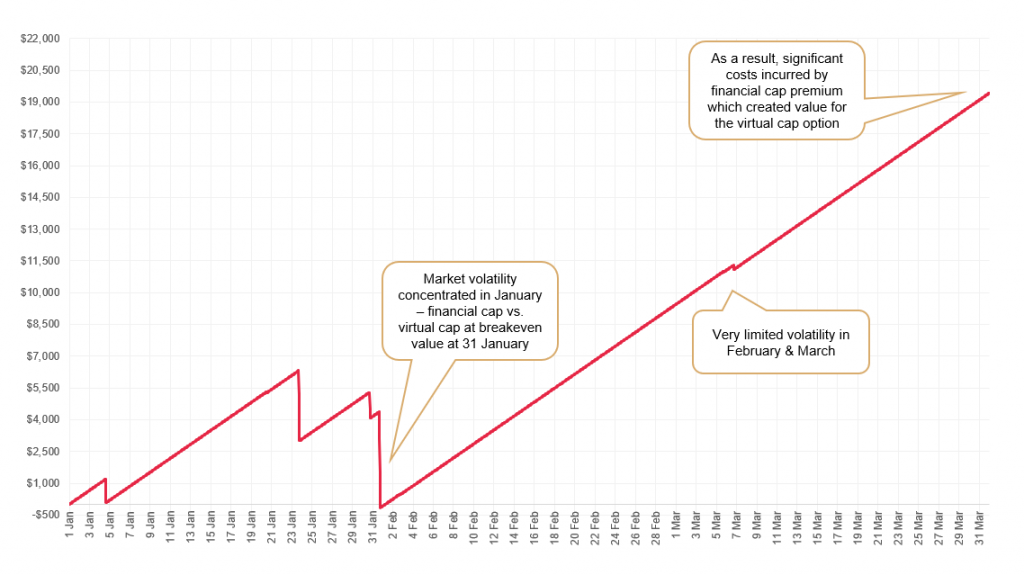

As seen in Table 1, market volatility as measured by the incidence of prices >$300/MWh was largely confined to the start of the quarter, with 15 out of 18 total intervals occurring during January. Of note, this resulted in the net value of the virtual cap being marginally negative as of 31 January. This was due to the income vs. premium cost to date of the financial cap being relatively balanced at that point, as well as the cost of the battery’s missed coverage during several high priced intervals. This trend is clearly illustrated in Figure 1 which shows the cumulative net value of the virtual cap (as per the above methodology) across the quarter. This highlights that the value to UQ was accrued in February and March where there were limited intervals >$300/MWh but the cost of the financial cap premium continued to be incurred, eroding the benefit of earlier payouts.

Figure 1: Cumulative net value of the virtual cap service across Q1

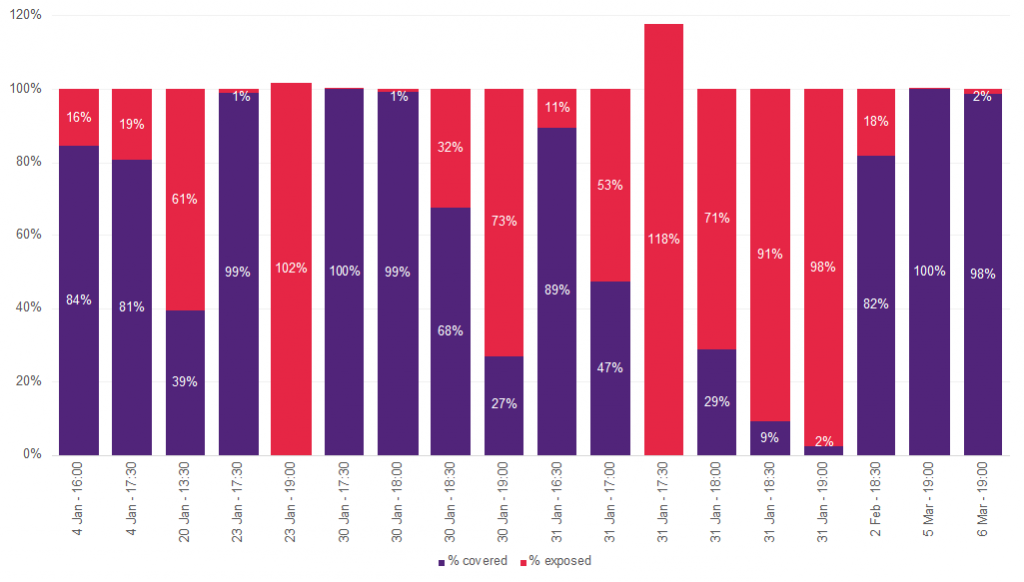

As shown in Figure 2, while overall volume coverage of 58% was achieved across the quarter, performance during individual intervals was highly variable. Most notably, the volume left uncovered during intervals on 23 January and 31 January exceeded 100%. This is due to the battery charging for at least part of the interval where the overall outcome should have instead been to discharge. Both of these events occurred as a result of erratic forecasts and a low state of charge that drove that battery to charge at what was at the time seen as a ‘cheap’ price in order to be ready for higher priced intervals that were forecast in the near future but did not eventuate. These outcomes provide a good illustration of the challenges faced by DRE’s control algorithm in optimising the battery’s performance during volatile periods and which are further discussed in the full report. As these two instances occurred when market pricing was $2,296/MWh and $1,610/MWh respectively, they had an outsized influence on the overall percentage of financial cover provided by the battery across the quarter. Excluding these two intervals the battery would have provided 66% volume cover and 73% financial cover.

Figure 2: Virtual cap volume cover performance during >$300/MWh intervals

Comparison to Wivenhoe Pumped Hydro

It is also possible to assess the battery’s performance against the major energy storage asset in Queensland – the Wivenhoe Pumped Hydro Power Station. With a pumping (charge) capacity of 2 x 252 MW and a generation (discharge) capacity of 2 x 285 MW, Wivenhoe is substantially larger than UQ’s battery. As a pumped hydro plant, its storage duration characteristics are considerably different than a battery, however it does not share the battery’s same ability to respond to market events in under one second. Most notably however, Wivenhoe is a major generation asset that is operated by a specialised energy company (CleanCo) with a dedicated trading team. This is compared to the UQ battery that is operated autonomously via DRE’s control algorithms. These factors accordingly make for an interesting comparison.

It is important to note that this comparison is not ideal. While performance data is publicly available, it is not possible to fully know why Wivenhoe traded the way it did. For example, it is likely that the CleanCo trading team also needed to consider how to trade Wivenhoe as part of their overall portfolio position in relation to aspects such as forward contracts that had been sold. Figures in the below analysis have assumed that pumping and generating at Wivenhoe occurs on a duty + standby arrangement, where only one pump or generator typically operates at a time.

| Wivenhoe | UQ Battery | |

| Charge MWh | 50,219 | 107.70 |

| Discharge MWh | 33,433 | 90.98 |

| Round-trip efficiency | 66.6% | 84.5% |

| Capacity factor (discharge only) | 5.4% | 3.8% |

| Capacity factor (charge + discharge) | 14.3% | 8.3% |

| Cap contract % volume cover | 74.9% | 57.9% |

| Cap contract % financial cover | 73.8% | 52.9% |

Table 2: Comparison of Wivenhoe and UQ battery across key metrics

As seen in Table 2, a large difference was observed between each asset’s effectiveness at providing cap coverage, with Wivenhoe achieving volumetric and financial coverage percentages in the mid-seventies range compared to the battery’s mid-fifties. This is likely a reflection of Wivenhoe’s vastly different storage duration characteristics, as well as the benefits of manual trading by experts. Notably however, the performance of the UQ battery is a lot closer to that of Wivenhoe if excluding the two intervals discussed above where inadvertent charging occurred. In this case, the battery would have achieved 66% volume cover versus Wivenhoe’s 75%, but would have almost matched Wivenhoe on a financial cover basis, with 73% coverage versus 74%. This highlights the importance of further optimisation of the DRE control algorithm which are discussed in the full report.

PS Thursday 14th May 2020 – UQ Report Released

————————————–

About our Guest Author

|

Andrew heads corporate Energy & Sustainability at the University of Queensland (UQ) and is Project Director of the 64 megawatt Warwick Solar Farm. He and his team are leading a world first initiative for UQ to become a 100% renewable ‘Gensumer’ – playing on both sides of the energy market as a large scale energy generator and large energy consumer, utilising energy storage and demand response to help deliver UQ’s operational energy needs in a flexible, sustainable, and lowest cost manner.

You can find Andrew on LinkedIn here. |

Thanks Andrew, sounds like a great project.

It looks a large amount of the value here is coming from realized spot prices underperforming traded cap premiums. I wonder if it would be possible to simulate outcomes from a quarter where the opposite occurred, such as Q117?

Totally agree Tom – the Q1 financial results were largely driven by relatively low levels of volatility compared to what the market was expecting before the start of the quarter. We will win some and lose some over time in this regard. The more important learning was how effective the battery was at providing ‘coverage’ against the baseline of 100% with a financial cap – approaching that levels of volatility will have an impact on this too from quarter to quarter. We were heartened by these results. Although the headline figures aren’t great (mid-fifties), if we’re able to tune out the issues we had with the control algorithm in the two rouge itnervals, the figures would be not far off what you’re able to achieve with a major generation asset (and cap seller) like Wivenhoe. Understanding what % coverage is plausible will help inform how much we can rely on the ‘virtual’ service in lieu of more traditional hedging techniques going forward when trying to prudently build a risk management strategy for each quarter. Of course 5 minute settlement will be a game charger for the effectiveness of batteries in this regard… although will still be faced with the problem of optimising the charge level!

Good read and made even more interesting to me having just read the Hydro Tas articles by Cameron Potter et alia observing that forecasting charge/discarge errors were less important with longer duration storage. I am still unclear how the battery can earn arbitrage and provide the cap service at the same time. Perhaps I’m reading too late at night. A gas plant can generate for the owner’s benefit when price is above SRMC and below the cap price and still be available (assuming gas supply) to supply the cap product. If a battery does the same thing it will sometimes be discharged during the price run up towards $300 and then be unavailable when called on to defend the cap won’t it?

Thanks David. You’re definitely correct that chasing arbitrage with a battery will sometimes leave the owner exposed when needing to defend cap positions due to the relatively short duration storage capacity available. This is where the trading strategy (either manual or algorithmic) is critical to try and get the coverage % as high as possible (but also not lose what may be otherwise good arbitrage spreads). It was interesting to me that even a long duration, manually traded asset like Wivenhoe only achieved a coverage %s in the 70s. The challenges of price forecasting and flow on impact to co-optimising the different services of the battery is discussed in depth in the full report, with a few case study days used to help illustrate these and the pros and cons of different approaches of trying to address.

Thank you David for sharing this analysis.

The caps contract are a financial edge,the BESS like a peaking plant are a physical edge. A physical edge has a capital cost that I think needs to be factored in the analysis to make the correct comparison between the two edges.