NEM power consumption increases 0.8%

Solar and energy efficiency account for 1% reduction in consumption

Greenhouse emissions fell by 1.3% in 2016

Renewables increase market share from 12.2% to 14.7%

Five renewable plants start operating and one fossil-fuel plant ceases

Summary

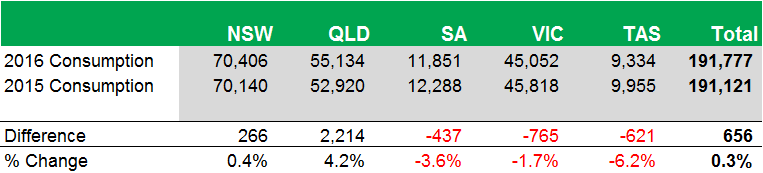

Electricity consumption in the National Electricity Market (NEM) increased by 0.8% in 2016, this is on top of a 1.1% increase in 2015. Queensland and NSW experienced increases in consumption with all other states experiencing a reduction.

We estimate that solar energy and energy efficiency activities supported by the Renewable Energy Target and various state based energy efficiency schemes reduced electricity consumption by 1,851 GWh. This is the equivalent of a 1% reduction in total consumption.

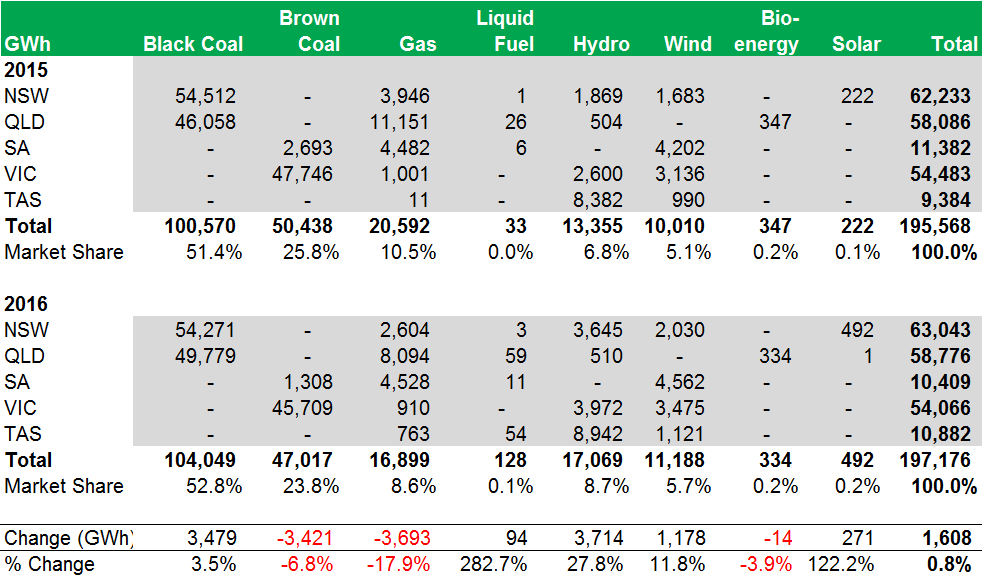

Renewable generation (excluding roof-top solar) accounted for 14.7% of total generation which was considerably higher than the 12.2% market share achieved in 2015. Hydro output increased by 27.8% and wind increased by 11.8%. Large-scale solar, whilst still relatively small is starting to register a growing contribution with five plants generating into the NEM in 2016.

Gas-fired generation dropped significantly again in 2016, falling by 17.9% on 2015 levels which in turn was 18.6% lower than 2014. Brown coal generation reduced by 6.8% due to the closure of the Northern Power Station in South Australia and lower generation from Victorian plants. Black coal generation increased by 3.5%, predominantly from Queensland generators.

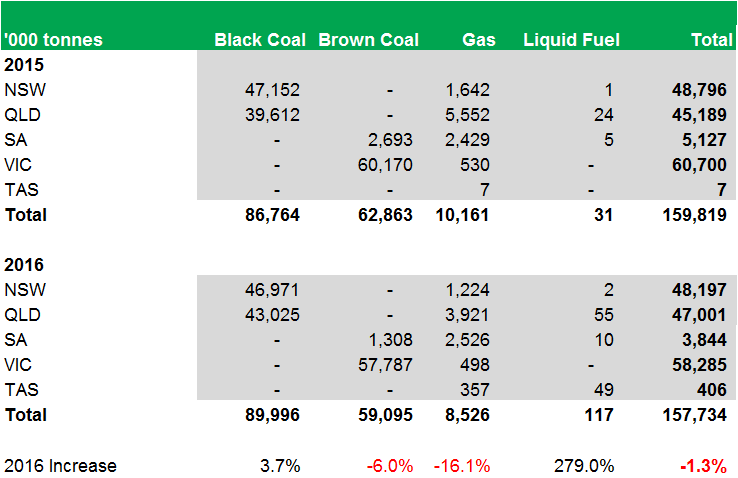

With lower generation from brown coal being replaced by an increase in black coal fired generation and renewables making up for the reduction in gas fired generation and increase in demand, NEM emissions reduced by 1.3%. The emission intensity of generation reduced by 2.1% falling from 0.817 tonnes per MWh in 2015 to 0.800 tonnes per MWh in 2016.

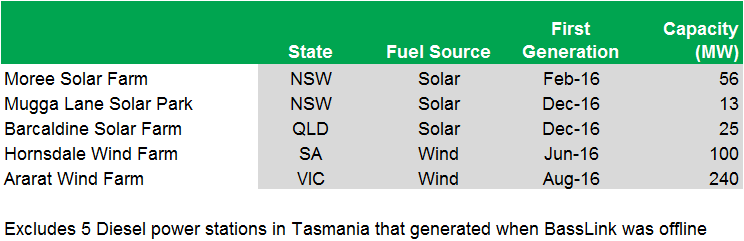

Six major new renewable projects above 10MW started generating for the first time in 2016; Hornsdale Wind Fam (SA), Ararat Wind Farm (Vic), Moree Solar Farm (NSW), Mugga Lane Solar Park in the ACT (included in NSW) and the Barcaldine Solar Farm in Queensland, as well as the Coonooer Bridge Wind Farm. Although Coonooer Bridge generation is not reported by AEMO and is missing from numbers reported here. The Northern Power Station in SA was the only significant fossil fuel plant to cease generating in 2016.

This Green Energy Markets Insight analyses the changes in electricity generation and consumption in the NEM for the year ending 31 December 2016 and compares it to the same period in 2015. Our analysis is based on scheduled metered demand and metered generation data published by the Australian Energy Market Operator (AEMO) and provided through Global Roam’s NEM-Review. The data does not directly measure actual consumption as it includes transmission losses, power station auxiliary use (power used in the power station) and excludes non-scheduled generation. As transmission losses, auxiliary use and non-scheduled generation have been fairly stable in recent years it nevertheless provides a solid basis for analysing year on year changes to electricity consumption.

1. NEM electricity consumption

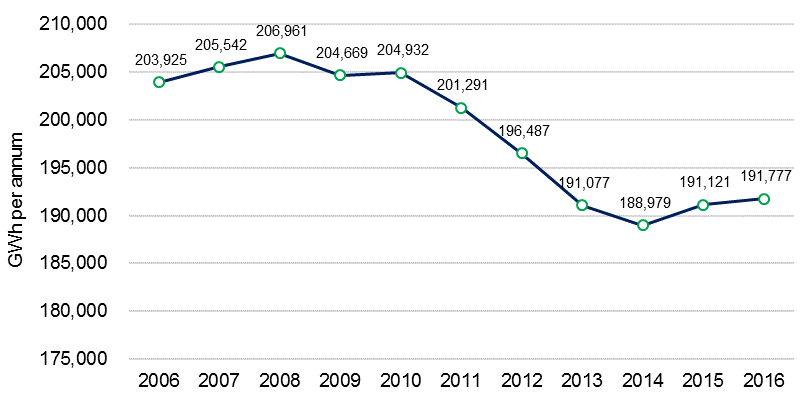

After declining for a number of years’ electricity consumption in the NEM (as measured by scheduled demand) continued its 2015 direction and increased by 0.8% in 2016 (refer to Figure 1).

Figure 1. Metered scheduled demand from 2006 to 2016

Underlying electricity consumption increased in Queensland and NSW (Table 1) with the other states experiencing a reduction in consumption. The continued start-up of the LNG plants explains a reasonable proportion of the growth in Queensland. The extended impact of the Basslink outage was predominantly responsible for lower demand in Tasmania.

Table 1 – Metered electricity demand by state – GWh (2016 cf: 2015)

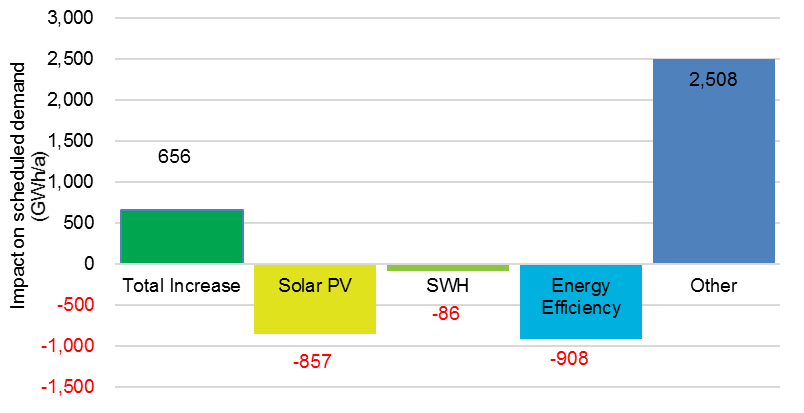

Approximately 620 MW a year of roof-top solar PV was installed in NEM states and created certificates under the Renewable Energy Target over the 2015 and 2016 period. This is estimated to have generated an additional 856 GWh in 2016 and appears as a reduction in scheduled demand.

The contribution of solar hot water and an array of energy efficiency activities supported by state based energy savings schemes have also contributed to lower electricity consumption. There are four energy efficiency schemes operating across the NEM; in NSW, Victoria, South Australia and the ACT. We have analysed the number of certificates or abatement that has been generated by a range of approved activities over the 2015 and 2016 period to estimate the full year impact. In total, identifiable energy efficiency activities could reasonably account for 909 GWh of demand reduction in 2016 (Figure 2).

We estimate that solar installations supported by the Renewable Energy Target and energy efficiency activities supported by the various state based schemes will have contributed 1,851 GWh in 2016, equivalent to a 1% reduction in total consumption for the year.

The impact of a variety of other factors such as population growth, economic growth, changes in manufacturing usage and weather contributed an increase of 2,508 GWh (1.3% of total consumption)

Figure 2. Contributors to changes in electricity consumption (2016 cf: 2015)

2. Power generation in the NEM

In analysing metered generation we have included all generators for which AEMO publishes generation data. This includes all scheduled generation and also larger non-scheduled generators which are predominantly hydro and wind generators. The total metered generation figures are thus slightly higher than the scheduled demand.

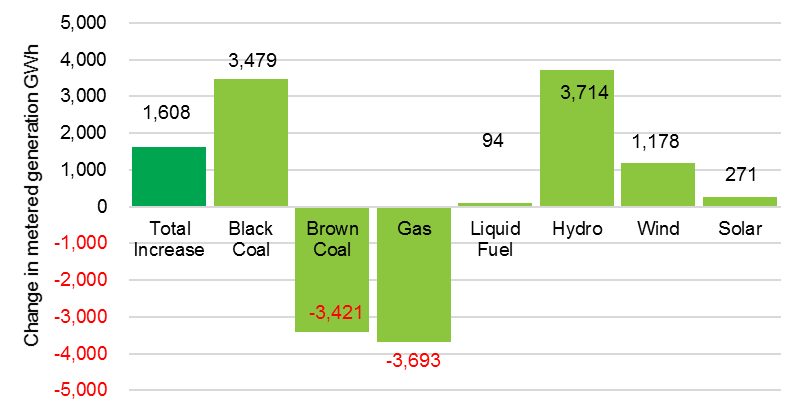

Changes in the generation mix in the NEM for 2016 are summarised in Figure 3. Hydro increased generation in 2016 by 27.8% after having fallen in 2015 by 8.2%. Snowy and Victorian hydro generators increased their output markedly, more than offsetting lower output from Tasmanian hydro generators. Black coal-fired generation in Queensland was responsible for the overall increase in black coal fired generation of 3.5%. Gas-fired generation dropped significantly in Queensland and NSW largely accounting for the overall reduction of 17.9%. The reduction in gas fired generation in 2016 comes on top of a 18.6% reduction in 2015. Over a two-year period, gas-fired generation market share has reduced from 13.1% in 2014 to 8.6% in 2016.

Figure 3. Differences in metered generation by fuel (2016 cf: 2015)

Wind generation increased by 11.8% in 2016. This was due to the commencement of the Ararat and Hornsdale wind farms and a full year’s output from the Bald Hills wind farm. In addition, 2016 was windier than 2015 with the average capacity factor for the year being more than 34% compared to 32% in 2015. Wind accounted for 44% of South Australia’s total generation in 2016, considerably higher than the 37% achieved in 2015.

Table 2 – AEMO metered electricity generation by state and fuel (2015 cf: 2014)

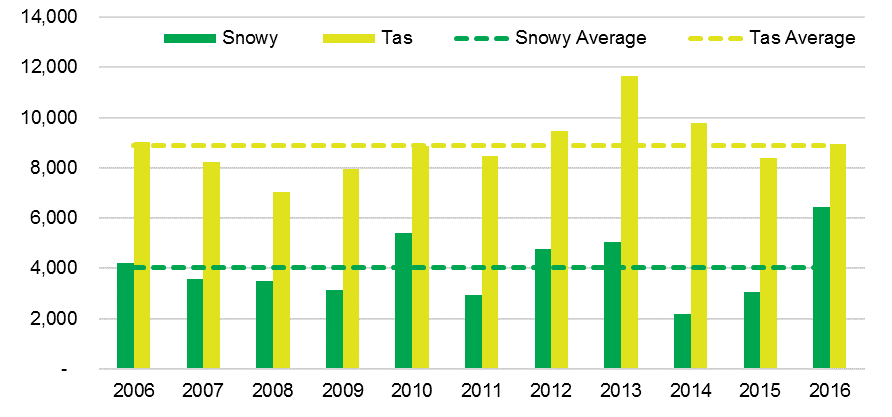

Snowy hydro generation in 2016 was more than double 2015 levels with Tasmanian hydro generation being 7% higher (Figure 4).

Figure 4. Snowy and Tasmanian Hydro historical generation levels

3. New generation projects

Five large metered renewable generators came on line in 2016, including three large solar power stations (Table 3).

Table 3 – New power projects that started operating in 2016

4. Generators that were closed or mothballed

The Northern Power Station was the only major fossil fuel power station to cease operating during 2016 (Table 4).

Table 4 – Power projects that ceased operating in 2016

5. Greenhouse gas emissions

Greenhouse gas emissions decreased by 1.3% in 2016 (Table 5). The emission intensity of generation reduced by 2.1% falling from 0.817 tonnes per MWh in 2015 to 0.800 tonnes per MWh in 2016. The reduced emission intensity was due to black coal replacing brown coal fired generation and a significant increase in renewable generation replacing gas fired generation.

Table 5 – NEM Greenhouse gas emissions by fuel (2016 cf 2015)

Notes and references:

- Electricity consumption data has been sourced from AEMO (NEM-Review) and reflects the level of scheduled generation required to meet that demand. This therefore includes power station auxiliaries and losses;

- The AEMO metered generation data includes scheduled generators and some of the larger non-scheduled generators. Smaller non-scheduled renewables are excluded and we estimate that this amounts to more than 3,500 GWh (1.8% of total generation);

- Roof-top solar PV is not included as a generation source and is included as lower electricity consumption;

- Emissions intensity data by NEM generator has been sourced from the ACIL Allen Report to AEMO dated 11 April 2014 “Emission Factors – Review of Emission Factors for use in the CDEII”; and

- State and fuel source classifications for generators has also been based on the ACIL Allen Report dated 11 April 2014.

|

Ric Brazzale is the Managing Director of Green Energy Markets and has more than 30 years’ experience in the energy sector.

Prior to establishing Green Energy Markets in 2008, Ric was the Executive Director of the Business Council for Sustainable Energy (BCSE), now the Clean Energy Council, and a leading advocate for renewable energy and energy efficiency markets in Australia. During this time, Ric was actively involved in the development and implementation of a broad range of solar energy and energy efficiency policies and programs, including participating on the Government’s initial REC Advisory Committee. Further background to Ric can be found on Ric’s LinkedIn profile. |

Thanks for this analysis.